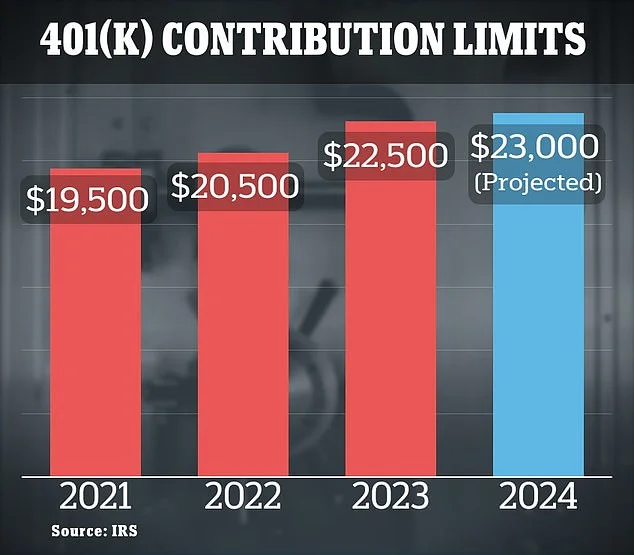

Alright, folks, buckle up, because something genuinely exciting just dropped: the IRS just announced the 2026 contribution limits for 401(k)s and IRAs, and they're way up. We're talking about a jump to $24,500 for 401(k)s and $7,500 for IRAs. But this isn't just about bigger numbers; it's about a seismic shift in how we think about retirement, and I, for one, am absolutely buzzing about it.

A Retirement Revolution

Think about it: for years, the conventional wisdom has been "work 'til you drop." Save a little, hope for the best, and maybe, maybe get to enjoy a few golden years. But what if that whole paradigm is about to get flipped on its head? What if, armed with these new contribution limits and a little bit of smart investing, a whole generation could be looking at early retirement?

The key here isn't just the increase itself, it's the compounding effect over time. Imagine, if you will, consistently maxing out your 401(k) at $24,500 a year, starting in your early twenties. Add to that the catch-up contributions for those 50 and older, now bumped to $8,000 (meaning a total of $32,500!), and you're looking at some serious firepower. This isn't just incremental; it's exponential, like the difference between a horse-drawn carriage and a rocket ship.

And for those slightly older, aged 60-63, that "super catch-up" contribution – still sitting pretty at $11,250 – is a golden parachute waiting to happen.

But here's where it gets really interesting: the SECURE 2.0 Act. It's not just about the headline numbers; it's about the fine print, the cost-of-living adjustments to IRA catch-up contributions. This is about building a system that adapts to real-world inflation, not some abstract economic model. It's a game-changer.

Now, I know what some of you are thinking: "Yeah, but what about inflation? What about market volatility?" And those are valid questions! But here's the thing: these increased limits are designed to outpace inflation. They're a hedge against the uncertainty of the future. It's like building a bigger, stronger ship to weather the storm.

And let's not forget about the income eligibility ranges for IRAs and the Saver's Credit, all ticking upwards. The IRS is essentially widening the gateway to retirement savings, making it accessible to more and more people.

Of course, as with any financial tool, there are nuances. Taxpayers can deduct contributions to a traditional IRA under certain conditions. However, if either you or your spouse is covered by a retirement plan at work, the deduction may be reduced – or phased out entirely – depending on your filing status and income. (But hey, if neither of you are covered, those phase-outs don't apply!)

This reminds me of the early days of the internet. Back then, people were skeptical. "It's just a fad," they said. "It'll never replace newspapers." But look at us now! We're on the cusp of a similar revolution, a retirement revolution, where financial freedom is within reach for anyone willing to seize it.

One thing we must think about, though, is the responsibility that comes with this. With greater financial freedom comes the need for greater financial literacy. We need to ensure that everyone has access to the tools and knowledge they need to make informed decisions about their future. It's not just about saving more; it's about saving smarter.

I saw a comment on Reddit the other day that perfectly captured this sentiment: "Finally, some good news! It feels like we're actually being given a chance to build a future." That's the spirit! This isn't just about numbers; it's about hope.

The Dawn of Financial Independence

What does this all mean? It means we're not just talking about retirement anymore; we're talking about financial independence. We're talking about the freedom to pursue your passions, to travel the world, to spend time with loved ones, all without the constant worry of running out of money. This is the kind of breakthrough that reminds me why I got into this field in the first place. The future is not something that just happens to us; it's something we create. And with these new contribution limits, we have the power to create a future that is brighter, more secure, and more fulfilling than ever before.